ฝันว่ามีลูกได้อุ้มลูก เป็นลางบอกเหตุต่างๆ ในชีวิต มันอาจจะเป็นลางดี มีมงคล หรือเป็นลางร้ายก็ตาม โดยเฉพาะ เซียนหวยหลายคนมักจะมีคำถามว่าฝันว่ามีลูกได้อุ้มลูก เลขเด็ดอะไร คุณมักจะสงสัยและอยากทำนายความฝันนี้หรือไม่ มาค้นพบคำตอบที่ถูกต้องที่สุดด้วยบทความข้างล่างกับ PIRA Inc นะ ฝันว่ามีลูกได้อุ้มลูก เลขเด็ด ตามความแบ่งปันของผู้ชำนาญในการแทงหวยและซื้อหวย แต่ละความฝันว่ามีลูกได้อุ้มลูกจะสอดคล้องกับเลขเด็กที่ไม่เหมือนกัน มาดูเลขเด็ดที่มีโอกาสชนะสูงซึ่งพี่น้องควรอ้างถึงกันนะ ฝันว่ามีลูกได้อุ้มลูก 1 คน เลขเด็ด 05 –

ตามโลกแห่งจิตวิญญาณฝันว่าได้พระเครื่องมีข้อความลึกลับมากมาย เพื่อให้เข้าใจมันได้คุณต้องรวบรวมรายละเอียดของความฝัน อีกทั้งความฝันยังส่งเลขนำโชคลาภพิเศษมาให้อีกด้วย ดังนั้นการฝันว่าได้พระเครื่อง เลขเด็ดอะไรดี มาดูกันในบทความต่อไปนี้ของ PIRA Inc นะ ฝันว่าได้พระเครื่อง เลขเด็ด โดยปกติแล้วความฝันแต่ละอย่างจะเชื่อมโยงกับเลขใดเลขหนึ่งหรือหลายตัวขึ้นไป พวกมันจะช่วยให้คุณได้รับโบนัสก้อนโตเมื่อเล่นหวย แต่ตัวเลขจะแตกต่างกันไปขึ้นอยู่กับสถานการณ์ในฝัน ต่อไปนี้เป็นบางกรณีเมื่อฝันว่าได้พระเครื่องที่คุณสามารถอ้างถึงได้ ฝันว่าได้พระเครื่องเก่า เลข 13 – 26 – 178 ฝันว่าได้รับพระเครื่อง จากผู้ใหญ่ เลข:

ฝันเห็นพระสงฆ์ 1 รูป ความฝันนี้มีความหมายทางจิตวิญญาณและปรัชญาแห่งชีวิตมากมายที่ต้องการบอกผู้ฝัน ในขณะเดียวกัน ความฝันยังบ่งบอกถึงชุดตัวเลขโชคลาภที่สามารถช่วยให้คุณเปลี่ยนชีวิตได้เมื่อแทงหวย หากต้องการทราบว่าความฝันเห็นพระสงฆ์ 1 รูปหมายถึงอะไรและเกี่ยวข้องกับเลขเด็ดไหน โปรดอ้างอิงจากบทความต่อไปนี้ของ PIRA Inc. ฝันเห็นพระสงฆ์ 1 รูป เป็นเลขเด็ดอะไร พระสงฆ์เป็นคนที่บวช โกนผม และ ปฏิบัติตามคำสอนของพระพุทธเจ้า พวกเขามักอาศัยอยู่ในวัดหรือศาลเจ้า สวดมนต์ทุกวัน การที่คุณฝันเห็นพระสงฆ์ 1 รูป นอกจากจะเป็นลางบอกเหตุแล้วยังบอกถึงเลขเด็ดหลายคู่อีกด้วย

เมื่อพูดถึงนกอินทรี เราจะนึกถึงเจ้าแห่งนกทันที ไม่เพียงเพราะขนาดที่ใหญ่เท่านั้นแต่ยังมาพร้อมกับความแข็งแกร่ง ความดุร้าย และ กรงเล็บที่แหลมคมอีกด้วย เมื่อพูดถึงนกตัวนี้ คุณจะนึกถึงความแข็งแกร่งและความกล้าหาญในทันที แล้วฝันเห็นนกอินทรีย์ เลขนำโชคอะไร หมายความว่าอย่างไร มาถอดรหัสความฝันนี้กับ PIRA Inc. ฝันเห็นนกอินทรีย์ เลขเด็ด ความฝันแต่ละอย่างมีเรื่องราวและลางบอกเหตุของตัวเอง มีความฝันที่แตกต่างกันมากมายและแต่ละความฝันจะนำมาซึ่งลางบอกเหตุที่ไม่เหมือนกัน เมื่อคุณฝันเห็นนกอินทรีย์และอยากหาตัวเลขที่แม่นยำที่สุดให้แทงหวย โปรดดูข้อมูลด้านล่าง: หากฝันเห็นนกอินทรีย์บิน เลข 98 – 988

การฝันเห็นสุนัข 2 ตัวไม่เพียงแค่มีข้อความมากมายที่เกี่ยวข้องกับอนาคตของคุณแต่ยังส่งสัญญาณถึงชุดตัวเลขเด็ดที่สามารถช่วยให้คุณเปลี่ยนชีวิตเมื่อเดิมพัน หากอยากทราบว่าฝันเห็นสุนัข2ตัวหมายถึงอะไร ตรงกับเลขอะไร คุณต้องพิจารณาจากแต่ละบริบทของความฝัน มาไขความฝันนี้กับ PIRA Inc นะ ฝันเห็นสุนัข 2 ตัวเลขเด็ด สุนัขเป็นสัตว์ที่คุ้นเคย ไม่เพียงแต่ฉลาดเท่านั้นแต่ยังซื่อสัตย์ต่อเจ้าของอีกด้วย หลายบ้านถือว่ามันเป็นสมาชิกของครอบครัวด้วยซ้ำ จากมุมมองของนักเล่นหวยมานาน การฝันเห็นสุนัข 2 ตัวไม่เพียงแค่นำลางบอกเหตุมาแต่ยังเกี่ยวข้องกับเลขเด็ดแทงหวยอีกด้วย หากคุณหลงใหลในการเดิมพัน คุณสามารถดูคำแนะนำต่อไปนี้เพื่อค้นหาตัวเลขนั้น ฝันเห็นสุนัข 2 ตัวเข้าบ้าน

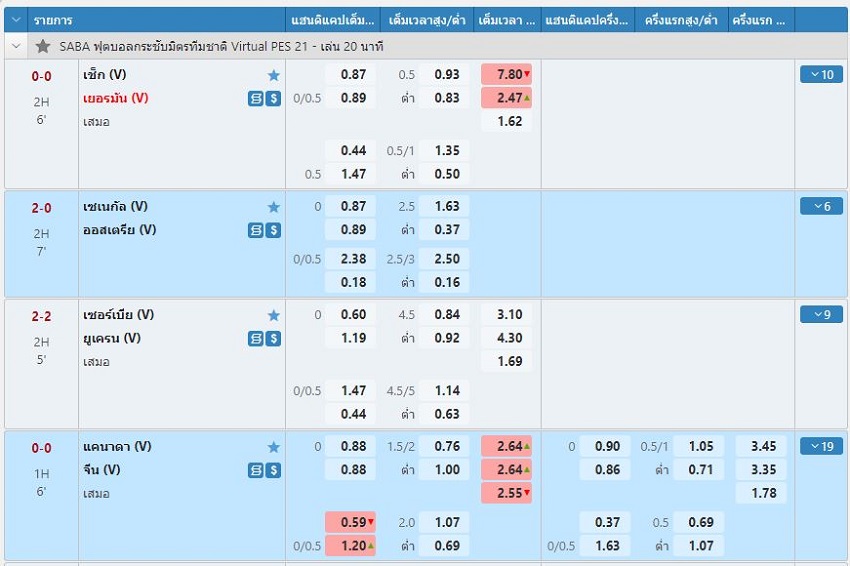

หนึ่งในการเดิมพันฟุตบอลที่พี่น้องหลายคนให้ความสนใจในปัจจุบันก็คือ ราคาบอลต่อเสมอ หรือราคาบอล 0 หากไม่เข้าใจว่าราคา บอล 0 คืออะไร หรือมีประสบการณ์ในการเล่นบอลแฮนดิแคปไม่มากนัก ไม่ต้องกังวล บทความต่อไปนี้จะช่วยให้คุณเข้าใจการเดิมพันประเภทนี้ครับ ราคาบอล 0 คืออะไร ผู้คนมักเรียกราคาบอล 0 ว่าราคาบอลต่อเสมอ หรือ แฮนดิแคป 0.0 นี่คือหนึ่งในประเภทการพนันฟุตบอลยอดนิยมของชาวเอเชีย เจ้ามือมักจะเสนอราคาบอลต่อเสมอในกรณีที่สองทีมแข่งขันกันเก่งเท่ากันหรือผลงานต่างไม่มานัก ดังนั้นอัตราต่อรองเป็น 0 นั้นสามารถเข้าใจได้ว่าไม่มีทีมไหนให้แต้มต่อ โดยปกติแล้ว

หากแทงบอลมานาน คุณคงคุ่นเคยกับ ราคาบอล 1.5 เพราะนี่คือราคาบอลนิยมที่เจ้ามือรับพนัน แต่ว่าผู้เล่นใหม่อาจจะยังสับสนกับราคาบอลประเภทนี้ ดังนั้น trong ในบทความนี้ Fun88 ทางเข้า จะช่วยผู้อ่านเข้าใจได้ดีขึ้นว่า ราคาบอล 1.5 คืออะไร และวิธีเล่นอย่างมีประสิทธิภาพ ราคาบอล 1.5 คืออะไร ราคาบอล 1.5มักจะปรากฏทั้งในเอเชี่ยนแฮนดิแคปและแทงบอลสูง/ต่ำ ก่อนเดิมพันอัตราต่อรอง 1.5 คุณต้องเข้าใจการเดิมพันประเภทนี้ ราคาบอล

ราคาบอล 2.5 เป็นประเภทการเดิมพันยอดนิยมในเอเชี่ยนแฮนดิแคปและแทงบอลสูง/ต่ำ ซึ่งเป็นที่ชื่นชอบและเลือกเล่นโดยผู้เล่นจำนวนมาก เนื่องจากการเดิมพันประเภทนี้ค่อนข้างปลอดภัยและมีโอกาสชนะสูง หากต้องการเรียนรู้เพิ่มเติมเกี่ยวกับราคาบอล 2.5 โปรดติดตามบทความด้านล่างของ PIRA Inc. ราคาบอล 2.5 คืออะไร ราคา บอล 2.5 คืออะไร ต่อไปนี้เรามาดูอัตราต่อรอง 2.5 ในการเดิมพันแฮนดิแคปและการเดิมพันสูงต่ำได้ที่นี่ ราคา บอล 2.5ในแทงบอลแต้มต่อ เช่นเดียวกับการเดิมพันแฮนดิแคป เจ้ามือเสนอ